Private equity still saw strong activity, even given the COVID-19 pandemic. In the world of private debt, the trend of larger fund managers closing on great-sized pools of capital remained. Now in 2021, fund managers will see rising demand from PE firms, halting other opportunities for capital deployment. View the full report here.

Executive summary

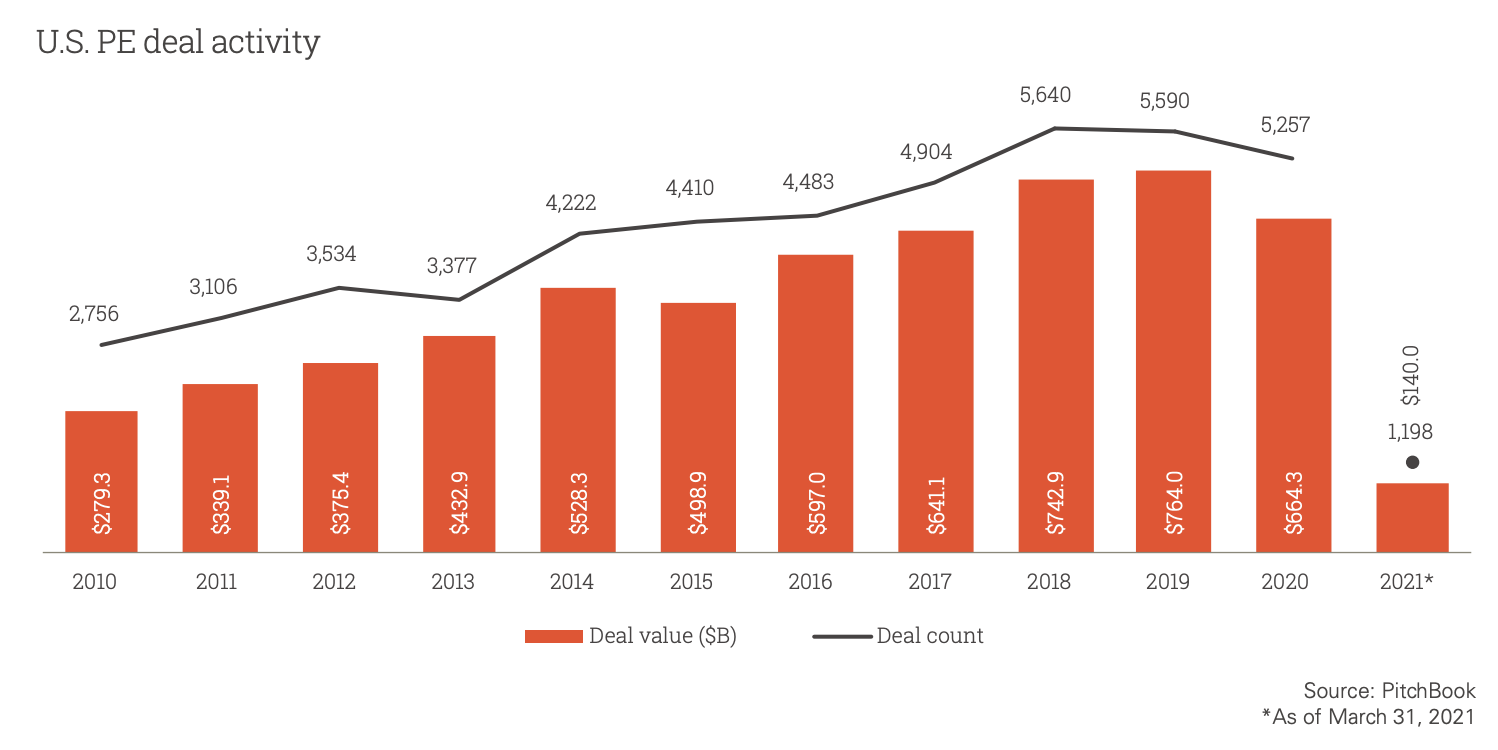

• Despite the COVID-19 pandemic, 2020 still saw robust private equity (PE) activity relative to historical activity, with well over 5,000 completed transactions even amid a drop in aggregate deal value to just over $664 billion. This healthy volume helped drive significant demand for private debt lending to PE portfolio companies.

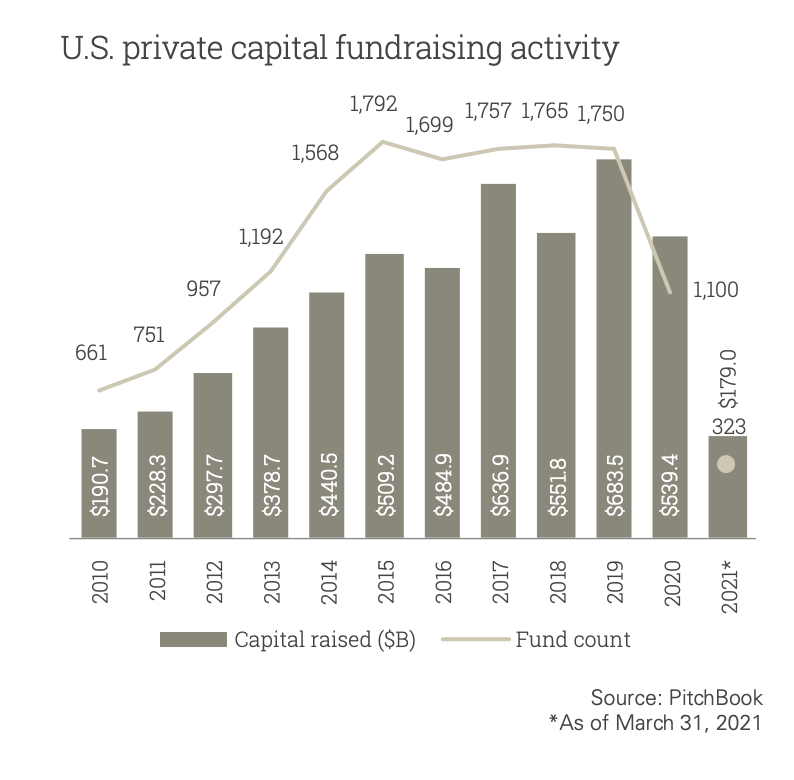

• Private capital fundraising, especially PE, still saw healthy levels of capital committed even as the tally of closed funds plunged.

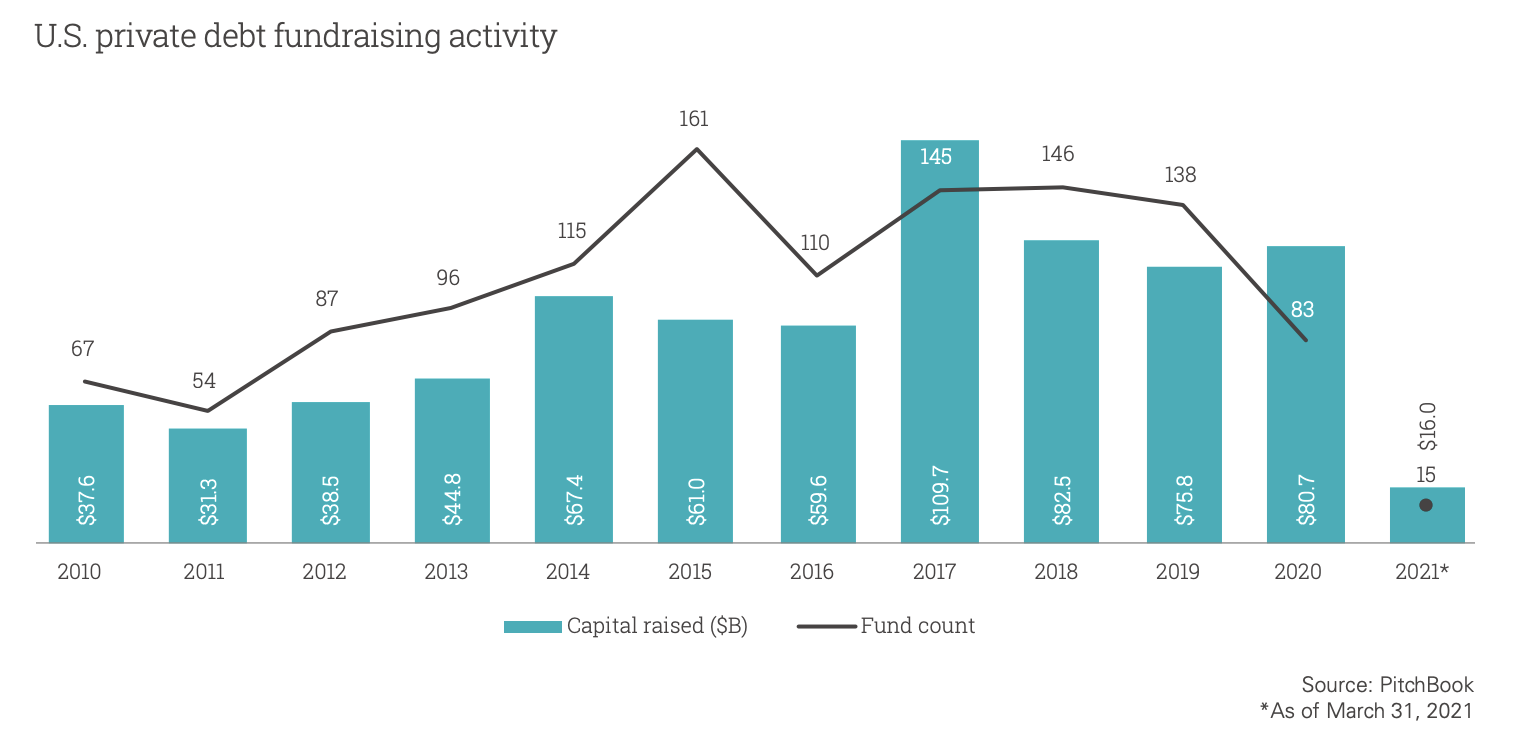

• The trend of more experienced and larger fund managers still closing on significantly sized pools of capital also held true for the private debt universe.

• Opportunism characterized trends in fundraising by strategy throughout 2020, with special situations benefiting, along with general debt, as PE fund managers sought bespoke financing solutions for portfolios and private debt players targeted distressed companies.

• Pandemic-driven drawdowns reduced record private debt capital overhang during 2020, but strong fundraising should help replenish.

• Heading into 2021, fund managers will face rising demand from PE firms and other entities given strengthening economic recovery with persisting dislocations, yielding further opportunities for capital deployment.

Overview: The private equity landscape

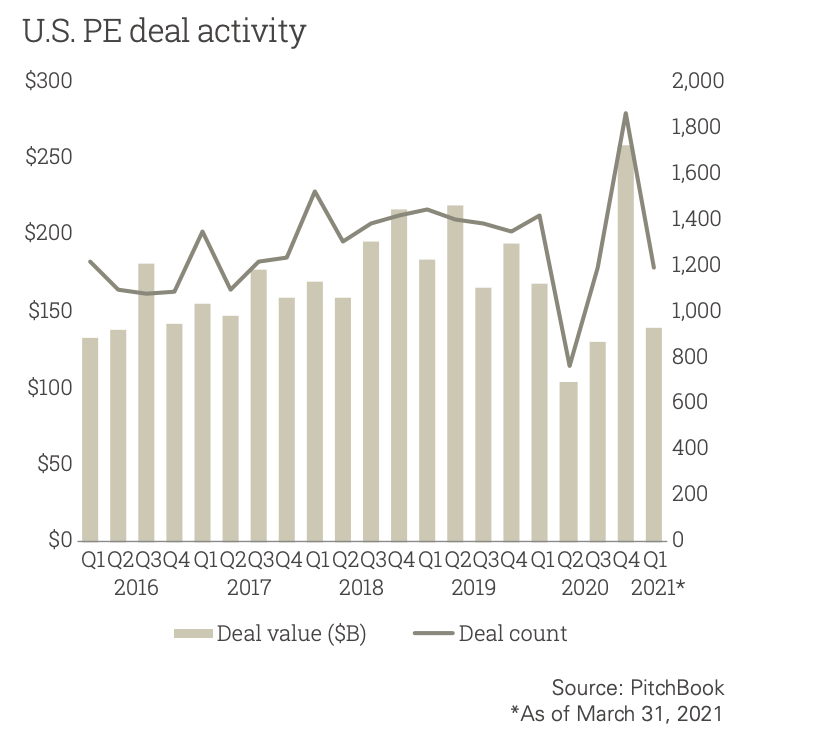

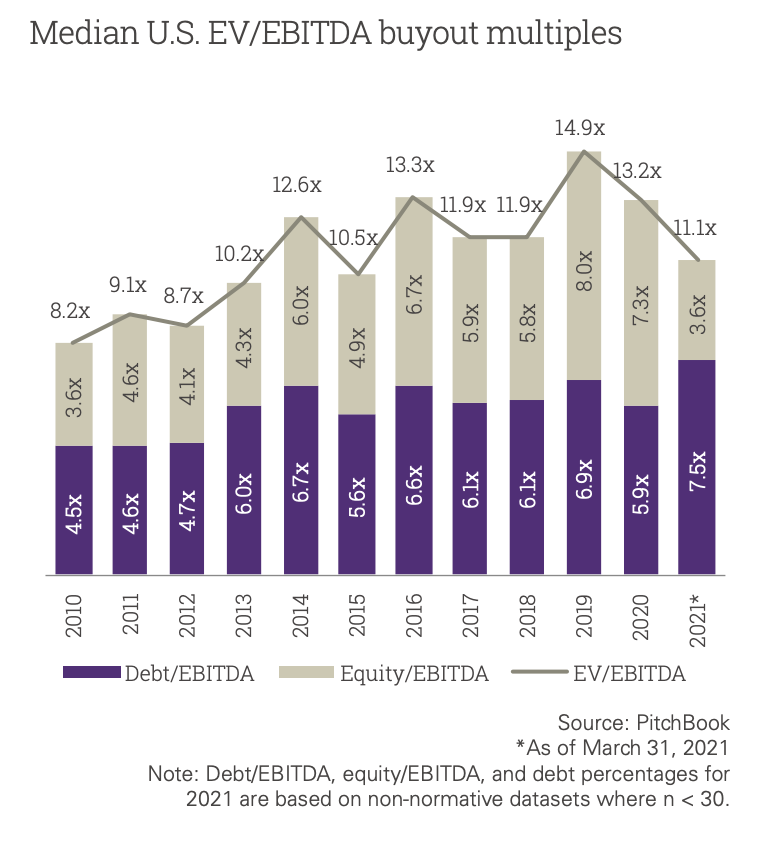

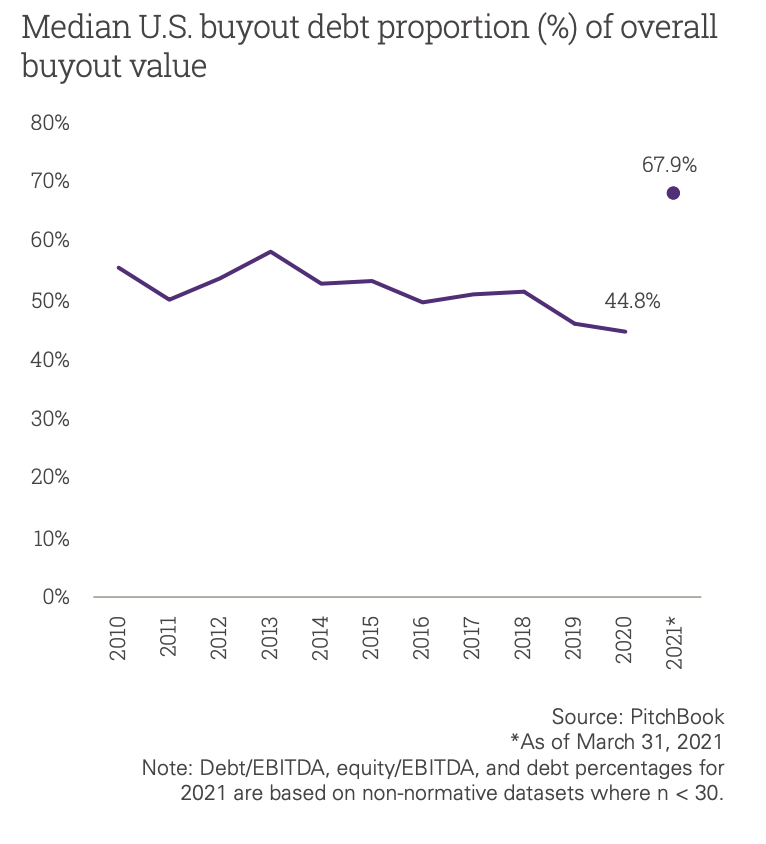

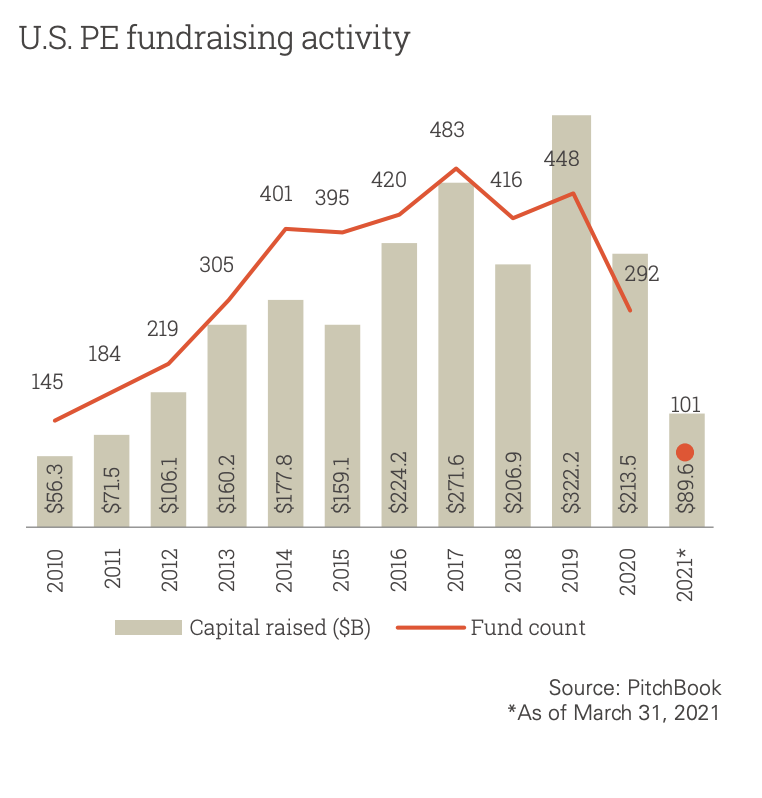

Even amid the tumult induced by the COVID-19 pandemic, PE dealmakers remained active. Although transaction volume declined year-over-year (YoY), and aggregate deal value fell markedly, 2020 saw relatively robust levels of investment. Quarterly data reinforces the temporality of the slowdown in dealmaking, with Q2 2020 experiencing a sharp, sudden plunge in deal count before the back half of the year saw concluded transactions come roaring back. Supported by the sheer heft of over a trillion dollars in committed capital, such vigorous dealmaking was accompanied by heightened demand for well-positioned companies, leading to buyout multiples remaining as high as ever and equity portions inching to a record (albeit based on small sample sizes). Record dry powder was a phenomenon long anticipated given the robust nature of past fundraising cycles, with 2019 seeing a massive $322.2 billion committed to U.S. PE funds. 2020 did see a sharp downturn in volume, but capital committed still exceeded $200 billion. All in all, the PE industry’s quick rebound in dealmaking helped drive significant demand for private debt. First, during the immediate onset of the pandemic, PE portfolios required shoring up and bespoke financing packages; second, as dealmaking roared back, fund managers tapped debt markets to close deals.

Current Trends in Private Debt

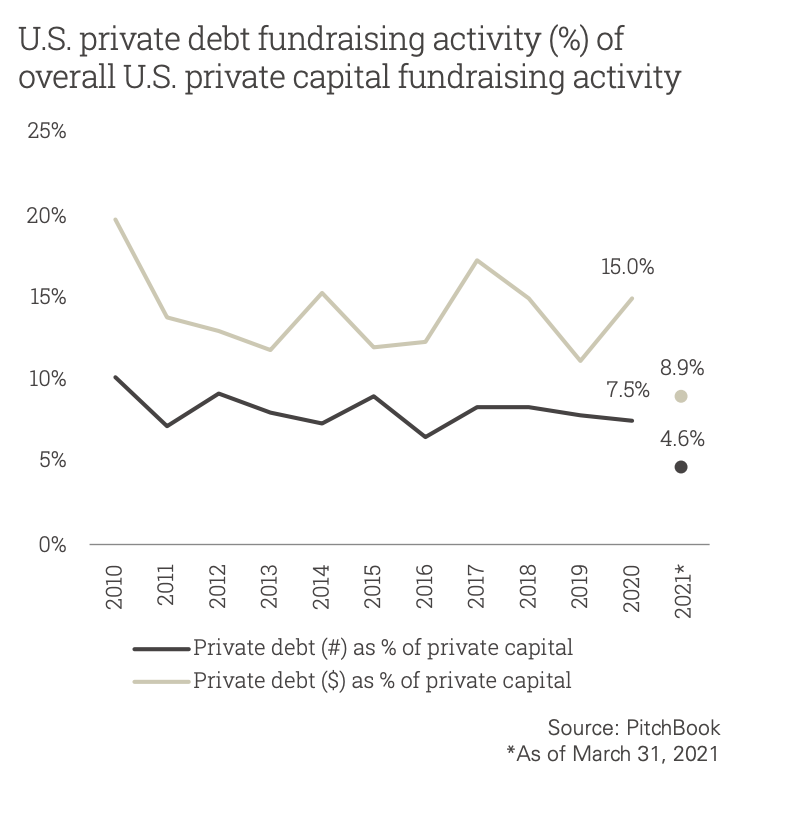

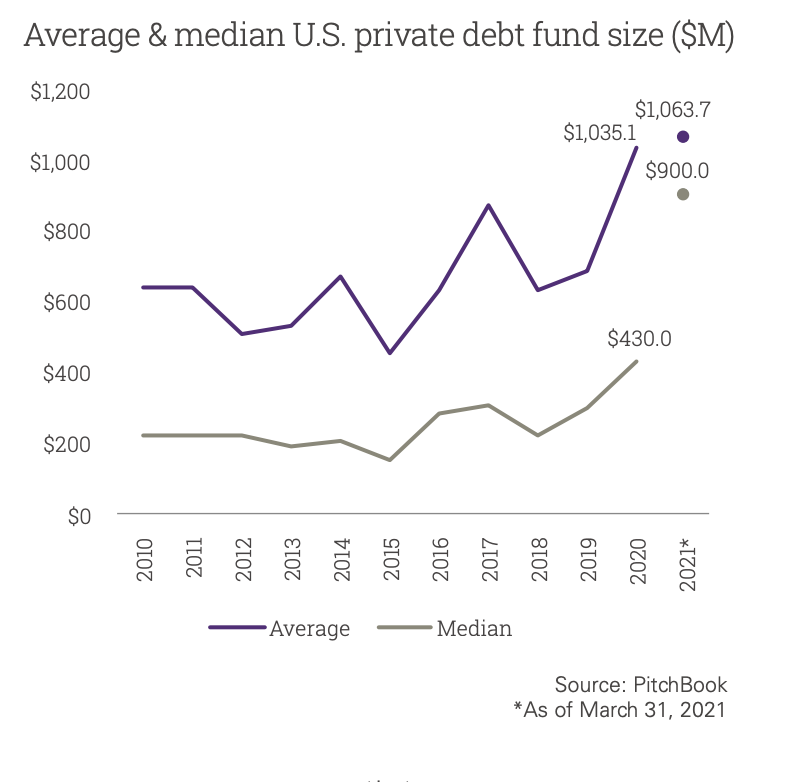

Private debt continues to steadily gain ground as an asset class. Its proportion of overall U.S. private capital fundraising volume held relatively steady over the remarkable environment of the past four years, with a spike in the percentage of overall capital raised to hit 15%. Despite the travails of the COVID-19 pandemic, when multiple fund managers faced significant challenges in portfolio management, private debt fundraising saw no less than $80.7 billion closed in 2020. However, the number of funds that raised that significant sum—the third-highest annual tally of capital committed to the strategy in the U.S.—almost halved, dropping from 138 vehicles in 2019 to 83 in 2020. Such a divergence was driven by many of the more experienced firms still closing on large pools of capital, touting their track record and capacity to handle the extraordinary pressures that many companies in their portfolios were experiencing due to the pandemic. Hence the surge in both the average and median private debt fund size between 2019 and 2020, both to record highs. Pulling all these trendlines together, there is still much room to grow and depth to be developed in the private debt market, although the unique nature of 2020 was bound to create a volatile environment.

Amid the funds closed, significant variances in fund type that could prove unique to 2020 emerged. Direct lending suffered a significant pullback in the volume of funds closed, while general debt and credit special situations grew. Opportunism explains much of the shift; however, direct lending had only held steady in terms of proportion of overall private debt fundraising volume for some years, whereas other strategies grew significantly. Direct lending’s unique characteristics—reliance on PE fund managers for origination, risk profiles, and so on—lead to pros and cons, one of the latter being more prone to one-off major risk events such as the pandemic. However, direct lending will likely return to relatively healthier levels of popularity in the future. It remains to be seen how other, more niche strategies fare.

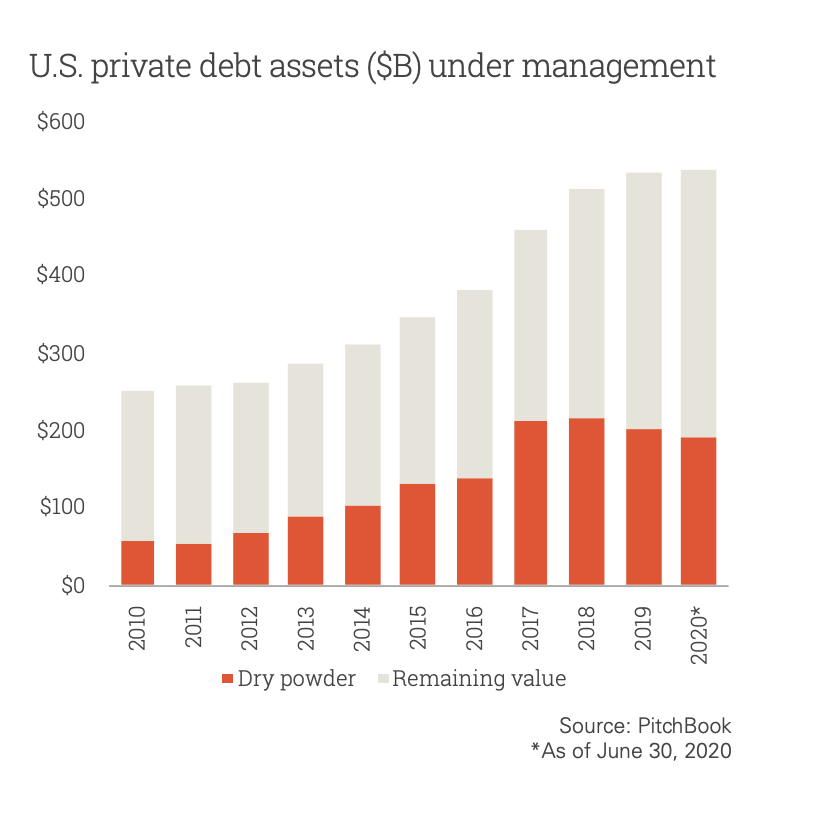

The same drivers that led to differing strategies enjoying sudden growth in popularity are also reflected in the drawdown in private debt overhang between 2019 and 2020, wherein multiple fund managers had occasion to restructure and support their various commitments and credit lines to ensure portfolio stability. This dip in dry powder also led to a noticeable jump in remaining value when decomposing assets under management (AUM). In turn, net cash flows from funds again turned into the negative territory after a slight positive surge in 2017. Notably, the three-year span prior to 2020 observed one of the stronger consistent tallies of distributions back to limited partners in private debt vehicles—a total of $209.7 billion. More recently, fundraising has outstripped such returns of capital by a fair degree, but that same popularity could yield a richer harvest in the post-pandemic environment, which will likely see persisting dislocations that could provide opportunities for private debt financiers to step in and supply capital.

Published July 21, 2021.